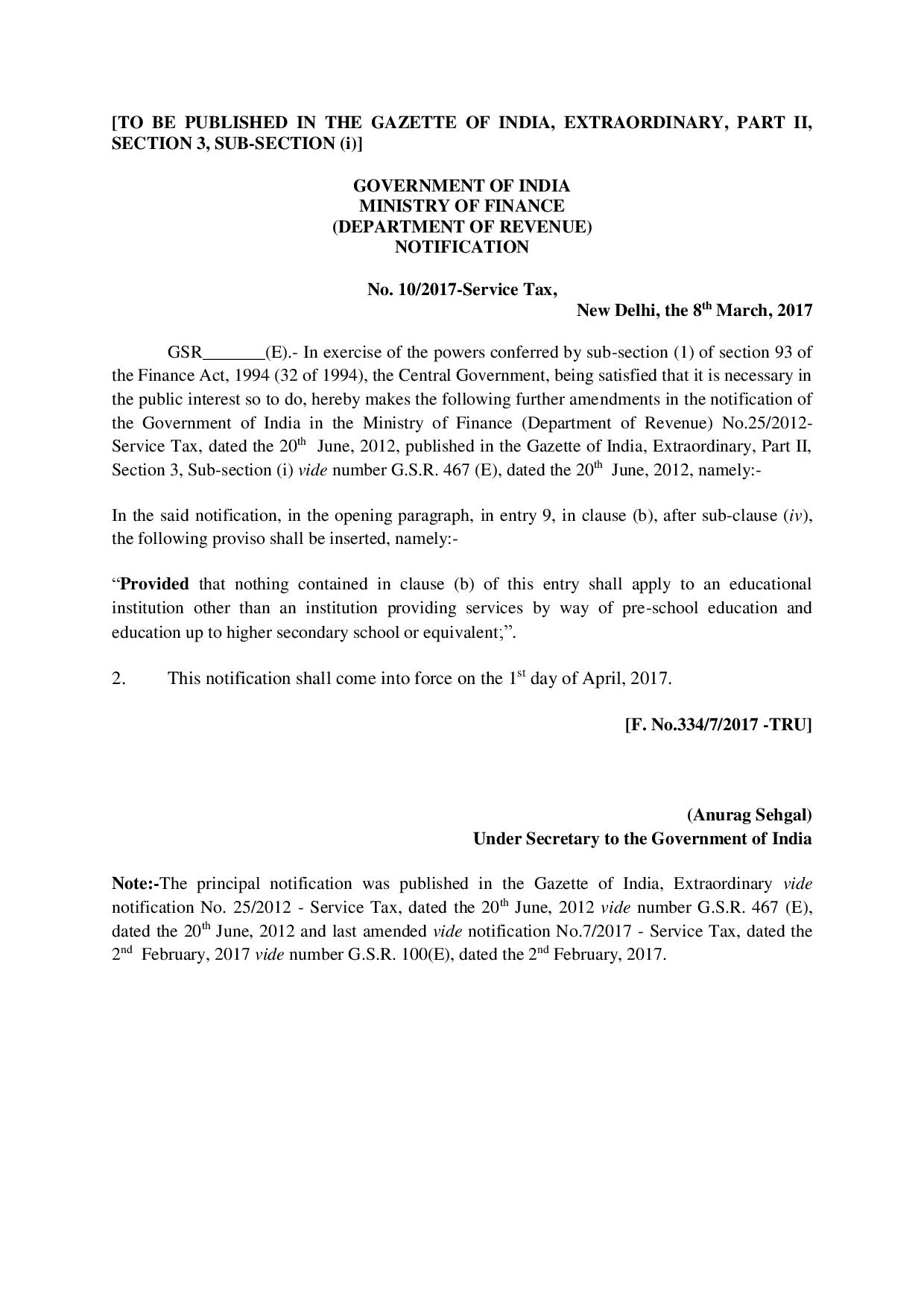

The Central Government has issued Notification No. 10/2017 – ST dated 08-03-2017 to add a proviso to Entry No. 9 (b) of the Mega Exemption Notification No. 25/2012. As a effect of the same the New Entry No. 9 (b) reads as below:-

9. Services provided, –

(b) to an education institution, by way of,-

(i) Transportation of Students, Faculty, and Staff;

(ii) Catering including mid-day meal sponsored by government;

(iii) Security or cleaning or housekeeping services;

(iv) Services relating to admission to or conduct of Examination by such institution;

“Provided that nothing contained in clause (b) of this entry shall apply to an educational institution other than an institution providing services by way of pre-school education and education up to higher secondary school or equivalent;”

1. These changes shall come into effect from 01st Day of April, 2017.

2. As an effect of this notification the services of Transportation/ Catering/ Security/ Admission or conduct of Examination provided to any college/University providing degree courses beyond higher secondary level will be taxable @ 15%.

3. It is important to note that there is no change in the position of law in cases where the Services are provided by an Education Institution to its student, faculty and staff and the same will continue to be exempted.

4. This notification has been introduced just before the rollout of GST and is a very strategic shift of the Government to Tax Education related services.

This has a major impact on the Colleges and Universities providing Degree and Masters level courses and they need to pay the additional liability of Service Tax in case of out sourced services received after 01-04-2017. For any further information or clarification in this matter, you can contact us on [email protected]